Adaptation & Resilience Metrics in Financial Decision-Making

Adaptation & Resilience Metrics in Financial Decision-Making

A Practical Approach for Financial Institutions

Financial institutions increasingly recognise that physical climate risk matters. The harder question is what to do about it, and how to justify adaptation and resilience (A&R) investment in ways that hold up in real decision processes.

This is where many financial institutions get stuck.

The issue is often not due to a lack of awareness, but a lack of decision-useful metrics. In practice, financial institutions often struggle to assess A&R outcomes consistently, compare options across sectors and geographies, or show how resilience improvements translate into financial relevance.

Cadlas is working with our clients and partners focus to close that gap – by developing a practical approach to A&R metrics that supports better investment decisions; not just better disclosures.

The Gap in the Market

Over the last half-decade, many financial institutions, supported by financial regulators and supervisors in numerous jurisdictions, have made meaningful progress on integrating physical climate risk assessment and disclosure into their operations. But progress on seizing the financing opportunities associated with A&R has been slower.

While A&R is increasingly recognised by financial institutions as strategically important, it is still often treated as a background issue in actual financing decisions. One reason is that financial institutions lack a usable way to connect three things that are usually handled separately:

![]() The improved A&R outcomes that an investment generates;

The improved A&R outcomes that an investment generates;

![]() The financial relevance of those outcomes to an investment or portfolio; and

The financial relevance of those outcomes to an investment or portfolio; and

![]() The pathways through which those improved A&R outcomes may affect financial performance.

The pathways through which those improved A&R outcomes may affect financial performance.

Without those connections, A&R remains harder to price, prioritise and structure.

What Financial Institutions Need Now

The case for why A&R matters is increasingly recognised. But to take action, financial institutions need metrics that are credible, practical and aligned with how decisions are actually made, as opposed to another high-level narrative.

Within financial institutions, different teams – operations, risk, sustainability, strategy – often have to answer questions in silos, with no shared analytical thread that connects them. Investment teams want to know whether there is a robust case for an A&R-relevant opportunity. Risk and structuring teams need to understand how A&R affects downside exposure and financing terms. Impact and sustainability teams need to evidence A&R outcomes in a way that is consistent and defensible. Strategy teams need to see where A&R fits within institutional mandates and longer-term market positioning.

A workable approach has to speak to all of these needs at once. That means bringing together public-good impact logic and private-good financial logic in a form that is usable in practice.

Cadlas’ Approach

Our work at Cadlas focuses on practical A&R metrics for financial institutions that are designed around the way investment decisions unfold in real life. We take a three-step approach to this:

1. Assess A&R impact

It starts with the basics: being clearer and more consistent about what positive A&R impact is being generated by an investment, for whom, and under what conditions. Despite sounding simple, in practice this is where many assessments become too generic to be useful.

It starts with the basics: being clearer and more consistent about what positive A&R impact is being generated by an investment, for whom, and under what conditions. Despite sounding simple, in practice this is where many assessments become too generic to be useful.

Our work in this area builds on existing good practices on impact measurement while focusing on making them more usable by financial institution. This means clear indicator selection, focused guidance for data-constrained environments, and templates that fit financial institutions’ due diligence and monitoring workflows.

2. A&R in financial decision-making

But measuring impact alone is not enough. Financial institutions also need to understand why that impact matters for financial decision-making. This means looking at A&R through a financial lens that operational teams within financial institutions – operations, risk, sustainability – can actually use.

But measuring impact alone is not enough. Financial institutions also need to understand why that impact matters for financial decision-making. This means looking at A&R through a financial lens that operational teams within financial institutions – operations, risk, sustainability – can actually use.

Rather than inventing entirely new metrics, this may entail using existing ones in A&R-informed ways to understand how A&R performance may affect downside scenarios, impairment risk, covenant headroom, insurance conditions, tenor, or other financing terms. This can make A&R legible within existing investment and credit processes, while identifying the residual cases where novel metrics are genuinely needed.

3. Connecting A&R impact with financial value

The final step is the one the market often talks about most but handles least rigorously: linking A&R impact to financial value. This is not the same as applying an A&R lens to financial metrics. It is about defining the pathway between the two: how public-good impact outcomes connect to value drivers, and how those value drivers connect to financial metrics, under specific conditions.

The final step is the one the market often talks about most but handles least rigorously: linking A&R impact to financial value. This is not the same as applying an A&R lens to financial metrics. It is about defining the pathway between the two: how public-good impact outcomes connect to value drivers, and how those value drivers connect to financial metrics, under specific conditions.

Our focus here is on disciplined linkage pathways, with explicit guardrails on where the linkage holds, where it is uncertain, and where it should not be assumed. In other words, the aim is not to imply that positive A&R impact automatically creates monetisable value, but to make the logic, evidence requirements and limits clear enough to support financial decision-making.

A key area of focus is Payment for Resilience Services (P4RS), building on Cadlas’ previous work with financial sector clients. P4RS is important here not simply as an example of A&R value, but as a mechanism for structuring the impact-to-value connection in practice. That includes defining A&R impact, setting verification triggers, designing payment mechanics, allocating risk, and integrating the approach into financing structures. Done well, this creates a clearer route from verified A&R impact to financial relevance in specific contexts.

Taken together, the aim is to give institutions a clearer basis for moving from A&R measurement to A&R investment.

Why This Matters for the Market

The financial sector is increasingly aligned that A&R matters – but awareness must lead to action. It needs better ways to evaluate, compare and structure A&R opportunities with confidence.

A more practical metrics approach can help institutions improve the quality and consistency of A&R decision-making, strengthen the financial case for A&R investment, and create a shared analytical language across the investment, risk and impact teams within financial institutions. That matters not only for individual transactions, but also for building more repeatable approaches at portfolio level.

As physical climate risks become more material across sectors and geographies, this becomes less of a niche sustainability issue and more of a core investment capability question.

Looking Forward

Through working with our clients on these emerging topics, our work at Cadlas is helping to bridge a persistent gap in the market: the disconnect between A&R impact assessment and financial decision-making.

By focusing on practical approaches that financial institutions can actually use in their decision-making, we can help to support better judgement, clearer structuring and more credible investment cases for A&R.

We warmly invite collaboration and exchange on these topics with interested stakeholders from across the financial sector or beyond. For further information on this area of our work, or to request an interview with a Cadlas specialist, please contact us at [email protected] .

Scaling Adaptation Finance through Country-Led Programmatic Approaches

Scaling Adaptation Finance through Country-Led Programmatic Approaches

Adaptation needs are rising rapidly as climate impacts intensify. While more countries are developing National Adaptation Plans (NAPs) and strengthening resilience components in their NDCs, a persistent gap remains between planning and implementation. A key challenge lies not only in the volume of finance, but in how it is structured, with fragmented project-by-project approaches struggling to translate national priorities into investment-ready pipelines at scale.

Against this backdrop, Cadlas supported the technical input to the policy brief Country-Led Programmatic Approaches for Scaling Adaptation Finance in LDCs and SIDS, developed by the NDC Partnership’s Center for Access to Climate Finance and the Global Green Growth Institute (GGGI). The brief draws on consultations with governments, development finance institutions, climate funds, and private sector actors to examine how country-led programmatic approaches can help structure and scale adaptation finance more effectively.

From planning to structured investment

Country-led programmatic approaches are increasingly seen as a way to move beyond fragmented funding toward integrated, nationally anchored investment frameworks. Cadlas previously explored this shift in our blog on national platforms for adaptation and resilience. The policy brief builds on growing global momentum around country-led programmatic approaches, including recent announcements at COP30 such as the launch of the Country Platform Hub, and examines how these approaches are being operationalized in practice across LDCs and SIDS.

At the core of the analysis is the Climate Investment Planning and Mobilization Framework (CIPMF), developed by the NDC Partnership and the Green Climate Fund. The brief uses the CIPMF as a lens to understand how countries can move from institutional arrangements to investment at scale.

The six stages of programmatic adaptation finance

The CIPMF outlines six iterative stages that help structure country-led programmatic approaches:

1. Investment Planning and Mobilization Capacity: Establishing governance arrangements, mandates, coordination structures, and core capacities to anchor adaptation within national systems.

2. Identifying and Prioritizing Investment Needs: Translating climate risk evidence and national plans into sequenced, high-impact investment priorities.

3. Financing Strategy: Mapping domestic and international public and private finance sources and aligning instruments with prioritized investments.

4. Programming with Finance Partners: Engaging development partners and private actors through structured dialogue to align pipelines with financing requirements.

5. Development of Projects and Programs: Converting priority areas into investment-ready proposals through standardized preparation and support mechanisms.

6. Project and Program Implementation: Channeling finance through national systems while strengthening monitoring, reporting, and learning processes.

Across case studies—including Bangladesh, Barbados, Brazil, Ethiopia, Jamaica, and Kenya—the brief shows that while models differ, certain features consistently matter: strong political ownership, anchoring in core institutions such as ministries of finance, structured stakeholder engagement, and investment in project preparation capacity.

What this means for adaptation finance

The analysis confirms that country-led programmatic approaches are not a universal solution. Structural constraints remain significant, particularly limited fiscal space, capacity gaps, lack of political appetite, and the continued dominance of project-based practices among financiers. Evidence of large-scale private finance mobilization for adaptation also remains limited. However, where designed carefully, these approaches can improve coordination across government and finance partners which strengthens the translation of NAPs and NDCs into structured investment pipelines; reduce transaction costs; align financing flows with nationally defined priorities and provide greater predictability across political cycles.

As global initiatives such as the Country Platform Hub and expanded GCF Readiness support reinforce this direction, country-led programmatic approaches offer a practical pathway for LDCs and SIDS to move from isolated adaptation projects toward longer-term, strategic resilience building.

Cadlas is pleased to have supported the NDC Partnership and GGGI in the development of this policy brief and to continue contributing to efforts that strengthen the systems underpinning adaptation finance.

The Launch of the Adaptation and Resilience Impact Measurement Toolkit

The Launch of the Adaptation and Resilience Impact Measurement Toolkit

Over the past year, Cadlas has worked closely with UNEP FI under the Climate Adaptation Innovation and Learning (CAIL) project’s Community of Practice on Climate Change Adaptation Impact Measurement and Information Flows (CoP4), exploring how information about climate adaptation and resilience (A&R) can be used by financial institutions.

An important message emerged from the extensive consultations with the broad range of financial institutions that make up CoP4: making the business case for scaling adaptation finance is more difficult when financial institutions cannot reliably measure or demonstrate the A&R impact of their financing activities.

When the benefits of A&R investments are not visible or verifiable, institutions struggle to build credible business cases for allocating capital to A&R. As a result, climate-vulnerable communities and sectors often remain unable to access the resources they need. Without systematic measurement, it is also harder to identify which interventions genuinely build resilience and which do not.

This Toolkit addresses this gap by providing a structured approach for assessing, tracking and communicating A&R impact. In response to this clearly identified need, over 2025 a collaborative effort between Cadlas, UNEP-FI and the CoP4 members has culminated in the development of the Adaptation and Resilience Impact Measurement Toolkit

Cadlas is proud to have contributed the technical inputs that shaped this Toolkit.

Drawing on our expertise in A&R impact measurement, we have helped to ensure that the Toolkit provides practical, decision-useful guidance that supports financial institutions in generating credible evidence of A&R outcomes and in integrating physical climate risk into financing strategies.

This forms an important part of our broader work here at Cadlas to help financial institutions embed A&R into their operations, pursue the opportunities associated with A&R as an emerging investment them, and scale up urgently needed finance for A&R.

The Measurement Challenge

As Cadlas has observed through our work with our financial sector clients, partners and stakeholders, A&R can be challenging for financial institutions to measure. A&R benefits can vary significantly across geographies, sectors and communities. Data in climate-vulnerable regions is sometimes limited, and it can often be difficult to establish counterfactuals against which A&R impact can be measured. Many A&R benefits unfold slowly, sometimes over decades, while financial institutions typically operate on much shorter investment and reporting cycles.

Together, these factors create an A&R measurement gap that constrains capital flows and contributes to the persistent under-valuing and under-scaling of A&R finance, even as climate impacts intensify. The Toolkit does not aim to eliminate these challenges entirely, but provides a practical framework that enables institutions to generate credible evidence of A&R benefits that is proportionate to their capabilities and decision needs.

The Toolkit is intended for to be used by a broad range of financial institutions including commercial banks, development finance institutions, insurers and reinsurers, and asset managers. It recognises that each institution type has different motivations, operational models and financial decision-making frameworks. To reflect these differences, the Toolkit includes institution-specific guidance that aligns measurement approaches with each organisation’s objectives and complements existing frameworks, enabling institutions to build on what they already use while filling gaps where more structure or clarity is needed.

A Clear Impact Pathway

At the heart of the Toolkit is the A&R impact pathway, linking financial inputs to outputs, outcomes and longer-term impacts

By concentrating on the stages where measurement is most feasible and reliable, the Toolkit helps institutions make the value of their adaptation and resilience activities more visible and more comparable.

It also draws on the logic of the UNEP FI Portfolio Impact Analysis Tool and introduces two complementary types of indicators, enabling organisations to track both their internal progress and the real-world A&R impact of their financing:

- Results indicators capture real-world A&R improvements delivered by financed activities

- Practice indicators reflect the internal processes, systems and capabilities that enable institutions to drive those results.

The Toolkit aims to provide an interactive starting point for financial institutions to begin generating and using these different indicator types as meaningful decision metrics across a range of financing activities and sectors.

Cadlas Senior Specialist and co-author of the toolkit, Noah Wescombe, notes the value of this approach:

What makes this toolkit uniquely useful to financial institutions is that it not only draws on diverse consultation from across the UNEPFI membership and its CAIL network but also provides a progressive approach to A&R measurement with multiple entry-points for organisations at different stages in their resilience journey.

Looking Ahead

While A&R measurement will always involve a degree of complexity, the Adaptation and Resilience Impact Measurement Toolkit offers a grounded and practical way forward. It supports institutions in identifying where physical climate risk matters most in their portfolios, what can be realistically measured and how this information can inform meaningful action.

The need for scaled up A&R financing is growing rapidly as climate impacts intensify and regulatory requirements increase. Financial institutions that strengthen their A&R measurement practices today will be better positioned tomorrow to scale responsibly, attract capital, manage risks and demonstrate genuine impact.

Cadlas looks forward to supporting our financial sector clients and wider stakeholders and partners to adopt and apply this toolkit, and to embed A&R measurement approaches and capabilities into their business practices and investment strategies.

Unlocking Adaptation Finance in ASEAN: The Launch of the mARs Guide Whitepaper

Unlocking Adaptation Finance in ASEAN: The Launch of the mARs Guide Whitepaper

The ASEAN region has made meaningful progress in recent years toward establishing a common language and framework for sustainable finance. At the centre of this effort is the ASEAN Taxonomy for Sustainable Finance (ASEAN Taxonomy), a classification system designed to guide capital flows into sustainable activities across ASEAN Member States (AMS).

The ASEAN Taxonomy aims to reduce fragmentation across jurisdictions, strengthen investor confidence and signal to markets and project developers which economic activities are likely to attract sustainable finance. While the taxonomy provides a solid foundation for advancing sustainable finance in the region, further enhancements to its usability and functionality for adaptation-specific purposes could play a significant role in unlocking additional investment for climate resilience.

To support this aim, the United Nations Environment Programme Finance Initiative (UNEP FI), the ASEAN Capital Markets Forum (ACMF), and the Sustainable Finance Institute Asia (SFIA) have released the Phase 1 Whitepaper on Key Principles and Methodological Approaches for the Development of the Mitigation Co-benefit and Adaptation for Resilience (mARs) Guide. This Whitepaper serves as the methodological starting point for developing the mARs Guide.

The mARs Guide is designed to complement the ASEAN Taxonomy by supporting users in conducting Environmental Objective 2 (EO2) assessments under both the Foundation Framework and the Plus Standard. It will outline the defining features of adaptation-related technologies and solutions within specific activities, including their purpose, role in adaptation, maturity, scalability, target beneficiaries, sphere of influence and potential environmental, social, and economic benefits including transformational impacts.

As Phase 1 of the mARs Guide development, the Whitepaper focuses on mapping national adaptation plans (NAPs) and related national strategies across AMS, along with reviewing international sustainable finance taxonomies and frameworks that address adaptation-related sectors. This mapping aims to identify shared principles, good practices, and methodological approaches that can be tailored to the ASEAN context. This ensures that the Guide is regionally relevant, evidence-based, and aligned with both local needs and global frameworks.

The Whitepaper also introduces a preliminary set of key principles to guide the design of the mARs Guide. These build on the five core principles of the ASEAN Taxonomy and the EO2 Guiding Principles, with added specificity for adaptation-related assessments:

- Science-based and evidence-led

- Context-relevant and locally prioritised

- Inclusive across ASEAN Member States

- Maladaptation risk management (uncertainty-aware)

- Interoperable and comparable

- Usable for finance and the real economy

Developed through extensive consultation with stakeholders across the region, including both users and providers of capital, the mARs Guide will supplement the ASEAN Taxonomy by clarifying what constitutes adaptation finance and how to assess resilience outcomes. In doing so, it reduces ambiguity, lowers transaction costs, increases comparability, and strengthens investor confidence. These improvements are essential for unlocking larger flows of public and private capital into climate adaptation projects and activities.

Cadlas remains committed to fostering a more resilient future by enabling informed, impactful investment in climate adaptation and resilience across ASEAN. We look forward to sharing further updates on how the mARs Guide will help transform the region’s sustainable finance landscape.

Resilience Unpacked: Investor Stewardship for Climate Resilience

Welcome to the third instalment of Resilience Unpacked, Cadlas’ insights series exploring key topics in climate resilience finance. In this edition, we explore how investors can use stewardship and engagement to drive climate resilience.

In Part 1 of this series on investor stewardship, we’ll look at how physical climate change impacts are emerging as a mega-trend for the investment industry and how responsible investment and climate resilience are increasingly integral to investors’ fiduciary duty.

As physical climate impacts intensify, investors are increasingly recognising the need to move beyond physical climate risk assessment and disclosure to support companies and assets in maintaining long-term value while adapting to a changing and more variable climate. In 2025, the World Economic Forum ranked extreme weather among the top risks to the global economy, while S&P Global estimated that the world’s largest companies could face annual costs of up to USD 1.2 trillion by 2050 due to physical climate risks. These figures underscore a clear message: the financial implications of a changing climate are material, measurable and mounting.

For the investment industry, this means adaptation and resilience can no longer be treated as peripheral sustainability issues. They must become central to how capital is allocated, how risks are managed and how long-term value is created and maintained.

Beyond Risk Disclosure

Over the past decade, the investment community has made meaningful progress in understanding and reporting on physical climate risks. Disclosure frameworks that cover climate scenario analysis, disclosure and risk assessment are now well established in a number of jurisdictions. However, most of these efforts still focus on assessing and disclosing physical climate risks, but often stopping short of responding to them. As climate impacts accelerate, investors will increasingly need to turn that analysis into action. This means using stewardship, including engagement with companies, influencing governance and exercising ownership rights, to build resilience within the companies and markets they invest in.

At its core, the shift is about turning climate awareness into climate action and recognising that resilience is not just a defensive measure, but a strategic imperative that protects and enhances long-term value.

Cadlas’ Investor Stewardship for Climate Resilience Sourcebook was developed in consultation with leading investors and investment industry associations to set out what this looks like in practice. It provides a blueprint that investors may use to embed physical climate risk considerations into their stewardship strategies and to work collectively to strengthen climate resilience across portfolios and markets. Importantly, it takes a pragmatic approach, offering pathways that investors can integrate into existing stewardship processes rather than creating entirely new initiatives.

Resilience and Fiduciary Duty

For investors, climate resilience is becoming an essential component of fiduciary duty. Acting with prudence and care in the face of physical climate risks requires understanding how those risks could affect assets, portfolios and broader market systems. It also requires supporting investee companies to anticipate, manage, and adapt to those risks effectively.

Reducing exposure to – or even divesting from – high-risk sectors or geographies may reduce portfolio exposure in the short term, but it can also undermine systemic resilience by cutting off capital from where it is most needed to build resilience. In contrast, maintaining engagement and using stewardship to encourage stronger risk management, adaptive planning and capital investment in resilience can drive both financial and social value. This approach parallels the logic of how responsible investment addresses decarbonisation challenges. Just as responsible investors understand that they need to stay engaged in hard-to-abate sectors to support low-carbon transition, they must also stay engaged in climate-vulnerable sectors to support their journey towards climate resilience.

However, investors’ approaches will differ based on their mandate, capacity, and risk appetite.

- Risk appetite: Investors with a higher risk appetite may choose to allocate capital to emerging resilience solutions or invest in companies operating in climate-vulnerable regions, recognising the potential for higher impact and longer-term value creation. Those with a lower risk appetite may instead focus on well-established resilience strategies or investments with more predictable risk-return profiles.

- Market of operation: Investors operating in markets that are highly exposed to physical climate risks may prioritise direct engagement with portfolio companies to strengthen adaptive capacity, while investors in more mature markets with stronger policy frameworks may focus on advancing market-level solutions.

- Size and capacity: Larger investors are often equipped to conduct detailed physical risk assessments, integrate resilience into governance and strategy, and lead collaborative stewardship initiatives. Smaller investors may need to prioritise the most material risks and leverage partnerships, pooled engagements, or service providers to extend their reach.

Whatever the approach, the key principle is consistency: ensuring that climate resilience is recognised as integral to fiduciary responsibility and long-term value creation.

- Integrate physical climate risk into investment policies, processes, and decision-making;

- Use robust data and scenario analysis to identify, understand, and manage material physical risks;

- Engage with portfolio companies and managers to strengthen governance, strategy, risk management, and disclosure around climate resilience;

- Identify and pursue opportunities that contribute to building resilience across markets and value chains; and

- Monitor, evaluate, and report on resilience performance and stewardship outcomes.

To explore this topic in more depth, download the Cadlas Investor Stewardship for Climate Resilience Sourcebook here or follow our Resilience Unpacked series on our website and our LinkedIn page. We welcome feedback on this topic and invite investors, policymakers and practitioners interested in advancing climate resilience through stewardship to connect with Cadlas at [email protected]

Stay tuned for Part 2, where we will unpack how investor stewardship for climate resilience can be applied in practice and explore approaches for structuring effective engagement for climate resilience.

Building Momentum for Adaptation Investment: Reflections from CAIP 2025

Building Momentum for Adaptation Investment: Reflections from CAIP 2025

Last week, Cadlas had the privilege of supporting the Asian Development Bank (ADB) in advancing its adaptation and resilience investment planning work at this year’s Climate Adaptation Investment Forum (#CAIP2025).

The conversations in Manila showed just how far the community of practice has come since we last gathered. Engagement was stronger, the discussions deeper, and the appetite for investment—both public and private—much clearer. There is clearly much more work to do, but to see this much progression and commitment to the process in only a year is very encouraging indeed.

We were honoured to have our own Noah Wescombe leading the conversation in two key sessions:

• Project Preparation Facilities for Adaptation – exploring how to design, structure, and scale the pipelines of projects that will ultimately mobilise finance, as well as the effective, sustainable models for maintaining PPFs for adaptation with national ownership.

• Country access to international markets and match-making – discussing how countries can unlock international capital and connect with private investors, while also noting the different levels of access and challenges faced in country readiness.

Both sessions gave us an excellent platform to share Cadlas’ recent work with ADB and the wider community, and to reflect on the lessons that can guide the next phase of CAIP’s growth.

Here are three of our key takeaways and lessons from #CAIP2025

• Country leadership is setting the pace. Certain countries are already innovating in policy, regulation, and practice. Their experience provides valuable lessons for others on how to overcome barriers and leverage opportunities.

• Private sector involvement is crucial. Public investment will remain essential, but we need more commercial banks, insurers, and investors in the room to bring scale and sustainability to adaptation finance.

• Metrics matter. Effective adaptation metrics are vital for planning and investment. If we can capture the financial as well as economic benefits of adaptation, we can give investors the confidence to commit capital.

Looking Ahead

At Cadlas, we see forums like CAIP as essential to turning ambition into action. The fact that adaptation investment is now firmly on the agenda (not just for governments and development partners, but also for private finance) is an encouraging sign of the shift underway.

We thank our colleagues at ADB, IIED, and across the CAIP community of practice for such a collaborative and inspiring week. We look forward to continuing to support this process, helping to translate national priorities into investable pipelines, and ensuring that finance is mobilised at the scale required.

Together, we can build a climate-resilient future—one investment at a time.

The Cadlas Sourcebook on Investor Stewardship for Climate Resilience

The Cadlas Sourcebook on Investor Stewardship for Climate Resilience: A Practical Resource for Embedding Climate Resilience into Investment Practices

After extensive consultations across the investment industry, Cadlas is pleased to announce the release of our Investor Stewardship for Climate Resilience Sourcebook. This new resource provides a practical framework for investors to align their stewardship practices with climate resilience goals. It lays out how investors can diagnose and understand physical climate risks, prioritise engagement with vulnerable companies and assets, and provide stewardship that drives the adoption of best practices on climate resilience across portfolios.

As the physical impacts of climate change intensify, investors face a defining challenge and opportunity. From floods and wildfires to water stress and heatwaves, physical climate hazards are becoming more frequent, more severe and more financially material. In this context, investors are increasingly recognising that identifying and disclosing physical climate risks is no longer enough. What is required is a shift from risk awareness to resilience action integrated directly into the way investors engage with the companies and assets they own.

The Investor Stewardship for Climate Resilience Sourcebook fills a critical gap in the market for tools and guidance that move beyond disclosure toward actionable investor engagement. It does not seek to reinvent existing investment processes, but instead demonstrates how climate resilience can be embedded within them through flexible and adaptive engagement strategies.

Importantly, the sourcebook builds on the growing body of work developed by leading investment industry bodies in recent years, aiming to advance action by focusing on the specific role investors can play in shaping a climate-resilient real economy.

This work emphasises that promoting climate resilience is aligned with investors’ fiduciary duties, encouraging investors to remain engaged and support climate resilience through targeted stewardship. It also highlights the need for tailored strategies across asset classes and geographies, while offering a curated toolkit of key resources.

By focusing on stewardship as a key instrument for advancing climate resilience, the sourcebook spells out how investors can strengthen long-term performance, manage systemic risks, and contribute to a more resilient and inclusive economy.

As physical climate impacts continue to grow in scope and scale, collaborative stewardship will be essential for unlocking the capital, capabilities, and influence needed to drive meaningful change. The time for passive risk management has passed. Through the release of this sourcebook, Cadlas hopes to contribute towards more widespread investor action that treats climate resilience not as a niche concern, but a core investment imperative.

The Investor Stewardship for Climate Resilience Sourcebook is available for download now.

Cadlas is also pleased to announce our upcoming webinar “Investor Stewardship for Climate Resilience” scheduled for 1pm (BST) on July 16th 2025. Sign up here and stay tuned for more info!

Sustainability-Linked Financing for Climate Resilience (part 2)

In Part 1 of this Resilience Unpacked series on Sustainability-Linked Financing for Climate Resilience, we explored the largely untapped potential of sustainability-linked bonds (SLBs) and loans (SLLs) to drive progress on climate adaptation and resilience. Despite their success in supporting mitigation goals, our research found that these instruments have only rarely been used to target adaptation outcomes. However, the growing application of water-related KPIs in SLBs and SLLs may offer a meaningful entry point for change.

In Part 2, we dig deeper into how water-related KPIs and SPTs are currently used in SLBs and SLLs across different sectors. We’ll examine how these indicators map against industry benchmarks, any emerging trends and practices shaping this evolving landscape.

Assembling the Evidence Base

To understand current practices, we analysed a dataset of 151 SLBs and SLLs issued between 2019 and 2024 that included water-related KPIs. This data was sourced from the Environmental Finance Database. Our research focused on four water intensive but key priority sectors: i) agri-processing, ii) manufacturing & services iii) property & tourism and iv) primary agriculture. After filtering out instruments from sectors outside our scope and transactions without disclosed KPIs, we identified 36 relevant SLBs and SLLs comprising 20 bonds and 16 loans for further analysis.

These transactions span a range of sectors and geographies, offering valuable insight into how water-related targets are structured in real sustainability-linked finance deals. They also provide a practical foundation for assessing the ambition and comparability of these targets against established industry benchmarks.

Anchoring to Benchmarks: What’s Available and What’s Missing

One of the key challenges in assessing SPT ambition is the absence of standardised benchmarks across sectors. To address this, our analysis drew on several existing reference points:

- EU BREFs

These are comprehensive, technical resources that detail the Best Available Technologies (BAT) for a plethora of industries. While the focus is on integrated pollution prevention and control across industries, they often include information on energy, water use and wastewater management. These documents offer granular, production process level industry benchmarks that, while useful, require careful interpretation to avoid misapplication outside their specific industrial context. As a result, we based our analysis on BREF water benchmarks.

- Buildings industry benchmarks

We referenced environmental benchmarks developed by the Better Buildings Partnership (BBP) to support our analysis of the property & tourism sector. These provide practical environmental benchmarks for commercial buildings, such as offices and shopping centres. However, their specificity to commercial buildings such as office blocks and shopping malls means they are not directly applicable to other building types like residential buildings.

- Food & Agriculture Organisation (FAO) resources

We reviewed water-related data and guidance from the FAO AQUASTAT database as well as other FAO resources to support our analysis of the primary agriculture sector. While rich in information, methodological uncertainties around target-setting in primary agriculture prevented us from fully integrating these benchmarks into our analysis.

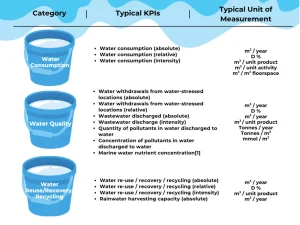

Water-Related KPI Categories in Practice

Our analysis revealed that water-related KPIs in SLBs and SLLs generally fall into three main categories: water consumption, water quality, and water reuse/recovery/recycling.

Water Consumption: These KPIs are the most widely used. These may be measured in absolute terms (e.g. cubic metres per year), in relative terms (e.g. percentage reduction in water consumption), or in terms of intensity – for example, water consumption per unit of product in manufacturing, per unit of activity in services, or per square metre in real estate. Some KPIs also focus specifically on water consumption from water-stressed regions, either in absolute or relative terms.

Water Quality: These KPIs tend to focus on the volume of wastewater discharged, either in absolute terms or in specific intensity terms and are commonly cited in BREFs. Some KPIs are qualitative and used to measure the wastewater pollutant load in terms of pollutant quantity or concentration.

Water Reuse/Recovery/Recycling: These KPIs are used in several sectors. These may be framed in absolute, relative, or intensity terms. A few transactions also include rainwater harvesting targets, although these are less common.

Table 1: Categorisation of water-related KPIs identified in the evidence base

Assessing Target Ambition: The Role of Second Party Opinions

In the absence of universally accepted benchmarks, SPTs in SLBs and SLLs are typically assessed by Second Party Opinion (SPO) providers. These providers use qualitative categories such as “insufficiently ambitious,” “moderately ambitious,” “ambitious,” and “highly ambitious” to rate the strength of a given target. While methodologies vary and are not always disclosed in full, two criteria consistently emerge.

First, SPOs often assess whether the target represents a meaningful improvement on the issuer’s past performance. This relies on transparent reporting of historic water use, which can be a challenge for some companies. Second, SPOs consider whether the target exceeds what is typical for the issuer’s sector. This comparative analysis depends on the availability of peer targets or recognised benchmarks, which are uneven across sectors.

Together, these criteria underscore the importance of both internal and external reference points in credible SPT design and the need for more consistent disclosure and benchmarking tools.

Sector-Specific Trends and Observations

The 36 SLBs and SLLs analysed reveal some important sector-level differences in how water-related KPIs and SPTs are used.

In the Agri-Processing sector, most water targets relate to consumption intensity, particularly in the beverage production sub-sector. Here, an ambitious target often involves a 10–20% reduction in water consumption intensity per unit (litre) of product. EU BREFs for the food, drink and milk industries also provide useful benchmarks for wastewater discharge intensity per unit of product, particularly in industries like brewing.

The Manufacturing & Services sector is highly diverse, spanning industries as different as pharmaceuticals, chemicals, paper & packaging, mining and logistics & services. Water KPIs here cover a broad range from water consumption in absolute terms in pharmaceutical production to wastewater discharge intensity in chemicals, plastics & rubber and paper & packaging, as well as water reuse/recovery/recycling in logistics & services. Given this diversity, setting credible targets requires deep industry-specific knowledge and benchmarking.

In the Property & Tourism sector, water consumption intensity is the dominant metric. Here, BBP benchmarks offer a relatively robust reference point for target setting. There is also at least one example of targets related to rainwater harvesting, although such these remain rare.

In contrast, the Primary Agriculture sector remains largely absent from the sustainability-linked finance landscape when it comes to water KPIs. Despite agriculture being the largest consumer of freshwater globally, our analysis found only one SPT in the livestock sub-sector, targeting absolute wastewater discharge. No examples were found for crop production despite it requiring the most significant amounts of water. While the ICMA KPI Registry provides many KPI recommendations, our research found little evidence of their practical use to set SPTs.

Looking Ahead

Our analysis across this Resilience Unpacked series highlights both the progress and the gaps in how water-related KPIs are used in SLBs & SLLs. While levels of rigour and benchmarking vary, what’s clear is that water offers a unique entry point for linking finance to resilience outcomes. Water is deeply connected to the impacts of climate change and increasingly measurable through performance-based metrics making it a natural candidate for integrating adaptation goals into mainstream financial instruments.

If we are to unlock the full potential of sustainability-linked finance for climate resilience, water-related KPIs could help lead the way. They offer a concrete, scalable foundation on which to build stronger, more credible frameworks that channel capital towards adaptation.

Thank you for following along with this Resilience Unpacked series on Sustainability-Linked Financing for Climate Resilience. Stay tuned for more from our Resilience Unpacked insights series and more!

Sustainability-Linked Financing for Climate Resilience (part 1)

Welcome to the second instalment of Resilience Unpacked, Cadlas’ insights series exploring key topics in climate resilience finance. In this edition, we examine sustainability-linked financing and its potential to support greater private investment in climate adaptation.

Results-based financing mechanisms such as Sustainability-Linked Bonds (SLBs) and Sustainability-Linked Loans (SLLs) tie financial terms to the achievement of sustainability goals. This creates incentives for companies to meet environmental performance targets. If structured around climate resilience-related Key Performance Indicators (KPIs), these instruments could channel much-needed private capital into adaptation measures at the corporate and entity level while setting powerful incentives for improving corporate performance on climate resilience.

Despite their growing popularity in supporting mitigation-focused corporate sustainability goals, SLBs and SLLs rarely incorporate adaptation and resilience objectives. This represents an underutilised opportunity to drive progress on adaptation and resilience. However, there may be important lessons from the application of sustainability-linked instruments in water-related investments that provide avenues for their potential role in financing climate resilience.

What are SLBs and SLLs?

Sustainability-Linked Bonds (SLBs) are general-purpose bonds that link financing terms, such as interest rates, to the achievement of predefined sustainability-related Key Performance Indicators (KPIs). If an issuer meets or falls short of its sustainability targets, financial terms may be adjusted accordingly.

Sustainability-Linked Loans (SLLs) function similarly but are structured as loans between a given lender and a given borrower, rather than bonds which are issued to raise funds from capital markets. Their terms also adjust based on performance against agreed sustainability KPIs.

Both instruments present an opportunity to incentivise investment in resilience by directly tying financing terms to progress on climate adaptation metrics. However, this opportunity has not been widely utilised across markets.

Limited Usage of Adaptation & Resilience Related KPIs

Despite the surge in sustainability-linked finance, adaptation KPIs remain strikingly rare. Research by Cadlas into global SLB issuances, using the Environmental Finance Database, found no examples of any specific adaptation or resilience KPIs included in global SLB issuances to date.

This trend was also observed in SLLs, with our research finding only one instance of climate adaptation as a KPI. HB Reavis, a UK-based real estate firm, secured a USD 32.4 million SLL in February 2024, which included a KPI linked to the number of EU Taxonomy-aligned buildings designed for climate adaptation. However, limited public information makes it hard to assess the robustness of this KPI.

This scarcity suggests potential uncertainty among issuers about how to define, implement, and measure adaptation KPIs. One key barrier is an unaddressed need for standardised guidance for adaptation-related KPIs in sustainability-linked finance.

Need for Clearer Guidance on Target Setting for Adaptation & Resilience

The International Capital Market Association (ICMA), a globally recognised standard-setting body, currently provides a limited number of KPIs that could convincingly be considered adaptation-related in the June 2024 iteration of its KPI Registry.

These are found in the Energy and Insurance (assets) sectors, representing only two out of ICMA’s twenty-six sectors. Within the Energy sector the adaptation-related KPI related to Share of energy produced in alignment with the EU Adaptation Taxonomy. While the KPI for the Insurance (assets) sector referred to the Proportion of invested assets managed with climate adaptation objectives.

Beyond these, ICMA lists three additional KPIs loosely linked to adaptation and all found within the Utilities (electricity) sector, but these lack clear resilience-focused outcomes. These include:

- Increase additional transformer capacity to facilitate interaction with the grid and integrate renewable energy generation,

- Increase power usage effectiveness/efficiency

- Renewable energy capacity (absolute or proportional).

This highlights the need for more detailed, targeted guidance on adaptation-related KPIs that are suitable for use in sustainability-linked debt instruments. Such guidance could build on existing best practices in financial sector adaptation and resilience metrics, such as the ARIC Adaptation & Resilience Impact Measurement Framework for Investors, developed in collaboration with UNEP-FI and Cadlas.

Water KPIs as a Proxy for Resilience in SLBs and SLLs

While adaptation-focused KPIs remain largely absent, water-related KPIs have gained significant traction, potentially serving as a stepping stone for broader resilience financing.

According to the Environmental Finance Database in 2024 there were:

- 43 SLBs valued at nearly USD 72 billion were issued globally with water-related KPIs by corporate borrowers

- The most common KPIs included water consumption reduction, efficiency improvements, and freshwater withdrawal reduction.

While several transactions did not specify precise bond KPIs, SLBs were categorised and grouped based on existing loan KPI details from the Environmental Finance Database and where possible, financing frameworks and other relevant publicly available documents.

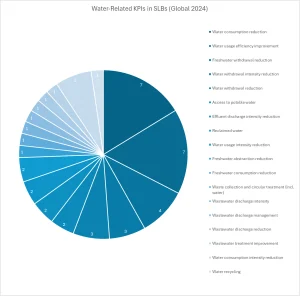

Water-Related KPIs in SLBs (Global Issuance, 2024)

The use of water-related KPIs appeared to be even more prevalent in SLLs, suggesting a stronger link between water management and this approach to sustainability-linked financing.

- 137 SLLs globally included water-related KPIs.

- The total lending volume of these SLLs reached USD 82.0 billion.

Of the one hundred and thirty-seven SLLs tagged by Environmental Finance as having water-related KPIs, only 121 could be categorised.

Water-Related KPIs in SLLs (Global Issuance, 2024)

Water-Related KPIs in the ICMA SLB KPI Registry

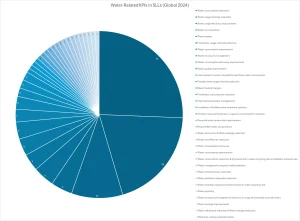

The water-related KPIs found in SLBs and SLLs from the Environmental Finance Database align closely with those listed in the ICMA SLB KPI Registry across a wide range of sectors including automotive, construction, energy, food and agriculture, finance, food & beverages, manufacturing, healthcare, maritime, metals & mining, retail, real estate, technology, transportation and utilities.

Across these sectors, water-related KPIs typically fall under six broad categories illustrated in the image below:

Six Categories in the ICMA SLB KPI Registry

These KPIs highlight the capacity for water to be used as a measurable, trackable and financeable resilience theme. However, while these KPIs offer a solid foundation, setting Sustainability Performance Targets (SPTs) against them remains a challenge.

From KPI to Impact: Driving Resilience & Improving Investor Confidence

Although water-related KPIs are common, the next hurdle is setting credible Sustainability Performance Targets (SPTs). SPTs tend to vary widely by issuer, sector and local context, and there is currently no standardised guidance for setting benchmarks or thresholds, especially for SLLs, where SPTs are rarely disclosed. This limits confidence and consistency across the market.

Despite this uncertainty around benchmarking & target-setting, SLBs still offer a powerful mechanism to incentivise financing broader resilience outcomes including water resource management.

The Anthropocene Fixed Income Institute (AFII) in their article ‘Rebuilding Confidence in the UK Water Sector,’ highlight the role SLBs can play in helping embattled UK water companies drive greater transparency on sustainability challenges, while also providing a financial hedge against poor performance for investors. AFII points out that by directly linking the cost of capital to measurable sustainability targets, water companies can improve investor confidence and build accountability.

Looking Ahead

At Cadlas, we are committed to driving innovation in sustainable finance that supports climate adaptation and resilience. One promising pathway lies in strengthening the design of SLBs and SLLs through more robust and relevant target-setting approaches. Developing clearer guidance for setting SPTs for water-related KPIs could be a practical and high-impact next step. This would not only reinforce the resilience link within SLBs and SLLs but also help build issuer and investor confidence in the adaptation value of these instruments.

By addressing these technical and strategic barriers, sustainability-linked finance can evolve into a more powerful mechanism for mobilising private investment in adaptation and resilience efforts. Water-related metrics, in particular, offer a compelling entry point for advancing this agenda. By anchoring SPTs in credible water-related KPIs, issuers can begin to demonstrate how sustainability-linked finance can deliver measurable adaptation outcomes. In doing so, they can help pave the way for wider market recognition of the role SLBs and SLLs can play in scaling climate resilience.

What’s Next?

In Part 2 of this Resilience Unpacked series on sustainability-linked finance, we’ll take a closer look at how water-related KPIs and SPTs are currently used in SLBs and SLLs across different sectors. We’ll examine how these indicators map against industry benchmarks, as well as analyse emerging trends and practices shaping this evolving landscape.

Insights from Resilience Unpacked: The Role of National Platforms in Unlocking Adaptation Investment

Insights from Resilience Unpacked: The Role of National Platforms in Unlocking Adaptation Investment

As climate risks intensify, the need to channel finance into adaptation has never been more urgent. Yet, despite more than a decade into formal national adaptation planning, implementation continues to lag behind. Cadlas’ recent webinar and panel discussion brought together leading experts Nanki Kaur from the Asian Development Bank (ADB), Michael Mullan from the Organisation of Economic Cooperation & Development (OECD), Bouke de Vries, independent expert and former advisor to the Executive Board of Rabobank and Danielle Evanson from the Government of Barbados’ Roofs-to-Reefs programme to explore how countries can and are already utilising national platforms to turn high-level adaptation policies into investment-ready strategies.

Unlocking the Potential of National Adaptation Plans (NAPs)

Nanki Kaur highlighted how National Adaptation Plans (NAPs) offer countries a structured way to assess climate risks and set sector-specific adaptation priorities. When done well, NAPs guide policy direction and investment planning, helping governments articulate both the urgency and strategic direction of their adaptation needs.

But turning these plans into investable projects is easier said than done. As Nanki pointed out, despite years of planning, adaptation financing remains elusive due in part to poor translation of climate risks into metrics that matter to investors. Many NAPs contain fragmented, small-scale solutions that fail to tackle adaptation at a systems level, and crucially, they’re often not well integrated into national public investment systems.

Making the Economic Case for Adaptation

Nanki also highlighted that one of the biggest challenges for countries has been demonstrating the value of adaptation. While there are many examples of economic modelling showing the costs of not adapting, very little analysis continues to be done on the benefits of proactive adaptation. This gap makes it harder for Ministries of Finance to justify adaptation investments or for private investors to see a business case for investing in adaptation.

To address this, ADB is supporting fourteen countries through its Climate Adaptation Investment Planning (CAIP) programme. This initiative focuses on aligning adaptation plans with public financial management systems and embedding economic analysis to assess the fiscal and financial returns of adaptation investment. This will in turn help governments to prioritise public funds where they are needed most, while steering viable projects towards private finance.

Building Institutional Architecture for Investment

Similarly, Michael Mullan underscored that effective adaptation planning requires robust cross-government coordination. While leadership often starts within specific ministries or agencies, unlocking finance and shifting national budgets requires collaboration from across all sectors and levels of government.

The OECD’s Climate Adaptation Investment Framework (CAIF) identifies six building blocks to integrate adaptation into investment planning including public finance mainstreaming, private investment support and sectoral regulation. To make this work, all parts of government need to be aligned. National platforms, Michael noted, can play a key role in strengthening institutional mechanisms, integrating climate risk into central government mandates and providing clearer planning signals to investors.

Lessons from Barbados’ Integrated Approach to Adaptation & Resilience

Danielle Evanson shared how Barbados is leading with an integrated, national platform approach through its “Roofs-to-Reefs” initiative. Rooted in the idea that climate resilience must stretch from households to coral reefs, the programme sits within the Prime Minister’s Office, enabling high-level coordination and oversight.

Roofs-to-Reefs operationalises adaptation planning by linking national policies, such as the Barbados Economic Recovery and Transformation (BERT) plan and Nationally Determined Contribution (NDC) with investment plans across six priority sectors including water, energy, waste, land use, ecosystems and housing. Importantly, this approach blends public and private investment, guided by a unified national vision.

Barbados has also turned to innovative financing tools to scale impact, structuring debt-for-nature and debt-for-climate swaps that mobilised investment from multilateral banks and domestic financial institutions. These mechanisms facilitated the establishment of the Barbados Environmental Sustainability Fund and the Blue Green Investment Bank, which is now in its operationalisation stage.

Engaging the Private Sector: Insights from the Netherlands

Bouke de Vries brought a unique perspective from the Netherlands Sustainable Finance Platform (SFP) convened not by a ministry, but by the Dutch Central Bank. The SFP aims to bring together stakeholders from the financial sector, government and scientific institutions to promote sustainability in the Netherlands. The platform makes recommendations for removing barriers to sustainable finance and is actively involved in pilots for sustainability initiatives.

In the SFP’s Climate Adaptation Working Group, members discuss what is needed to accelerate climate adaptation at the national level, with a particular focus on private sector stakeholders. Notably, this working group also includes the secretariat of the National Delta Programme’s commissioner.

Bouke highlighted that climate change poses a systemic risk which also affects the financial sector. It must therefore understand and manage these risks within its assets and client portfolios, with banks, insurers and institutional investors assessing, pricing, transforming, or avoiding them. Additionally, the financial sector contributes to adaptation and resilience by financing adaptation investments and insuring against risks. These are also important commercial opportunities.

Clear labels and taxonomies provide both urgency and clarity by helping to translate climate data into meaningful signals for market actors that can inform investment decisions. Well defined and actionable national adaptation strategies and targets are much needed to make adaptation more investable and bankable, as well as communication to businesses and people to raise awareness, enabling regulation and policies.

A Systems Shift Is Underway

If there was one overarching theme from the panel, it’s that climate adaptation can no longer be treated as an isolated policy issue. It must be understood as a systems issue, one that spans ministries, markets and entire economies.

Whether through national platforms like Barbados’ Roofs-to-Reefs, cross-sectoral coordination frameworks championed by the OECD, or regional investment planning supported by ADB, the shift from planning to financing adaptation is gaining traction. But for these efforts to succeed, countries must not only clarify their priorities they must also build the economic and institutional foundations that enable investment to flow.